Introduction

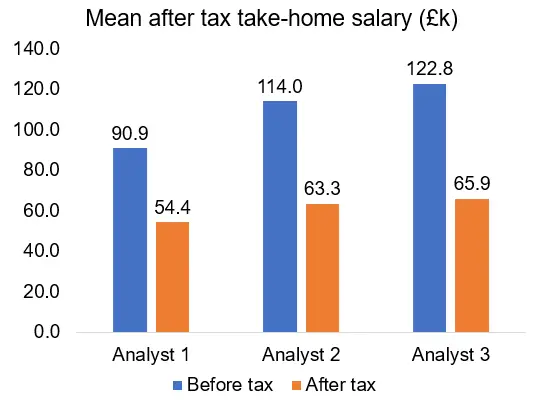

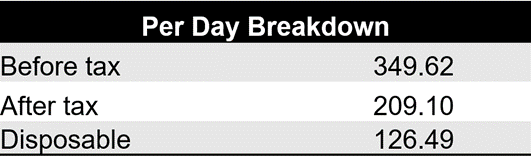

According to Dartmouth Partners data on Bulge-Bracket bank salaries, an investment banking analyst might expect to earn a base of £50.3k and a bonus of £40.6k before-tax, which translates to a total of £54.4k after-tax or £209.10 per day in their first year of work. When accounting for average living expenses, an analyst might expect to be left with £32.9k per year or £126.49 per day. Naturally, this salary increases as analysts gain more experience and move up the ranks although there is greater variation in salary further up the hierarchy.

I didn’t want to write this article and have put it off for a long time because the aim of this website is not to create the wrong motivations for those of us wanting to enter/entering the industry. However, I have now decided to write this post for the following reasons:

- Salary is still an important consideration when weighing up career decisions and rationalising the hundreds of hours of preparation that will be required for breaking into and working in investment banking.

- Much of the information on the web around IB salaries is either outdated or not London-specific enough.

- This post will give me the opportunity to highlight caveats that will prevent us from diving into this topic with the wrong mindset whether standing outside or inside the industry.

If you still want to apply to Investment Banking after reading this post, be sure to check out the divide and conquer strategy laid out below that comprises the “Intern Game Plan” for the most actionable and concise advice in the field:

- CV. Finalizing your CV and then boosting it e.g. by completing online courses so that you can apply early.

- Cover Letters. Writing a solid cover letter or pre-application question response through honing your communication skills and using insights gained through networking.

- Online Tests. Practising and documenting situational judgement and psychometric tests (numerical, verbal and logical).

- Video Interviews & Competencies. Developing an unbeatable set of competency question responses, cracking the HireVue video interview algorithm and first round interview.

- Technicals. Never getting caught out on a technical question.

- Commercial awareness. Building a repertoire of responses to ‘tell me about a recent news story’ and ‘tell me about a recent deal’.

- Assessment Centres (AC). Preparing for ACs which includes answering brainteaser questions and being able to present a killer PowerPoint deck.

- Resilience. Focusing on your circle of influence in the face of rejection while preventing application season burnout.

Side notes:

- The figures I include in this post may not be 100% accurate because things are changing very quickly in the industry continuing from the momentum sparked by the “Working Conditions Survey” from 13 Goldman Sachs employees, alongside strong industry tailwinds. I have decided to focus on sources that everyone can access to favour reliability over word-of-mouth updates.

- Although everyone is invited to read this post, I would say it is most suitable for those on the fence about whether to go into investment banking or currently applying to firms and contemplating whether this is the industry for them.

- I have mainly focused on Analyst 1 salaries since I believe it is the first few years that should be of primary concern for anyone entering the industry and data points become less reliable at more senior levels. After Analyst levels, there is the Associate level, after which is the Vice President level, followed by Director and Managing Director.

Average Base + Bonus

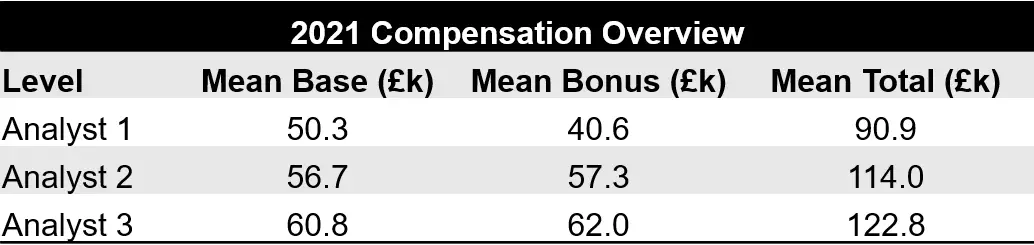

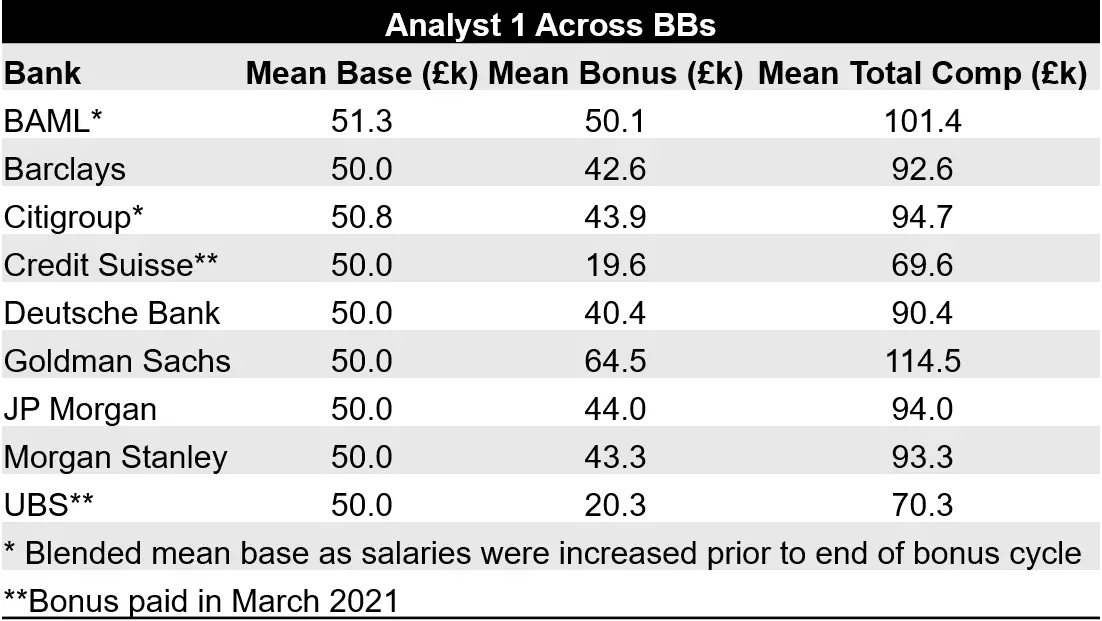

The salary figures featured in this post are sourced from the Dartmouth Partners 2021 compensation report which can be accessed here. Below I have listed a table summarising the mean base, mean bonus, and mean total salary from analyst 1 to analyst 3 serving as a useful proxy for the industry at large, followed by a breakdown of how these salaries vary across different bulge bracket banks.

Differences Between Banks

After-Tax Considerations

Here are the after-tax statistics using TheSalaryCalculator website, accounting for 5% pension contributions and assuming you took out a student loan and will be paying this back under repayment plan 2. Repayment plan 2 is for those of us who live in England or Wales that used the student loan and whose course started on or after 1st September 2012.

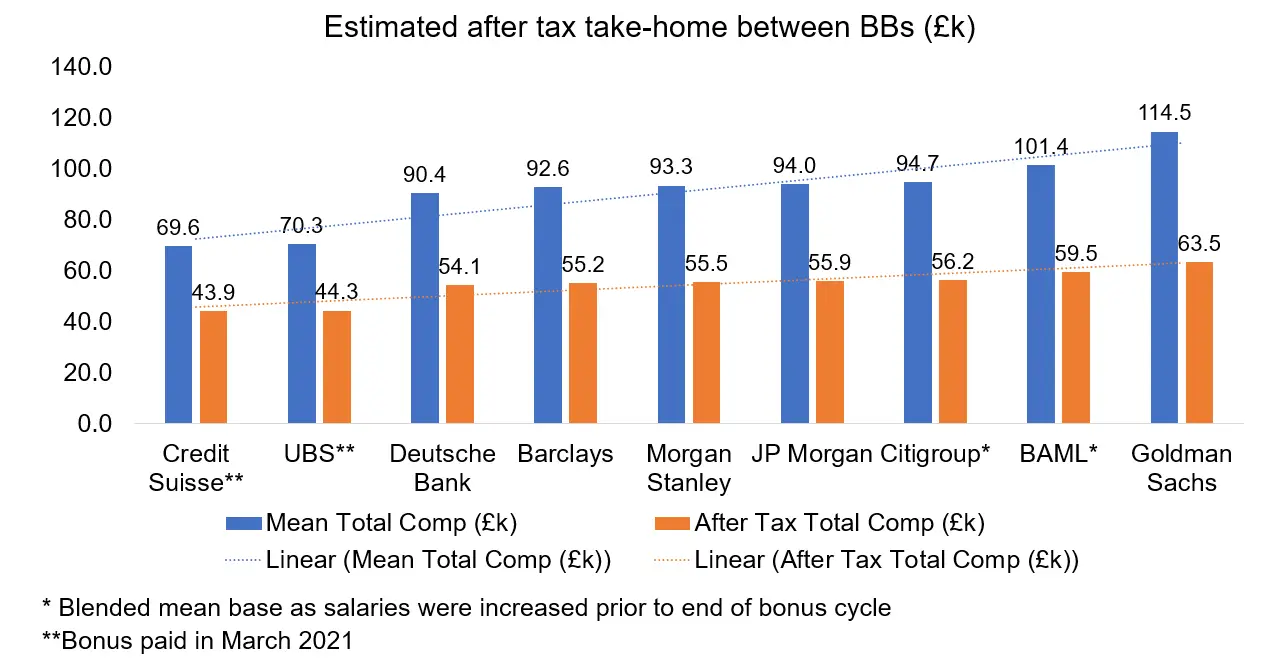

From looking at the graph below, you can see that after-tax, what initially seems like a large difference in salaries is massively dampened between banks. This dampening effect which is illustrated by the linear after-tax line would be even greater if Credit Suisse and UBS were removed, which were taken from March 2021 before the larger increases took place across the industry.

After Living Expenses

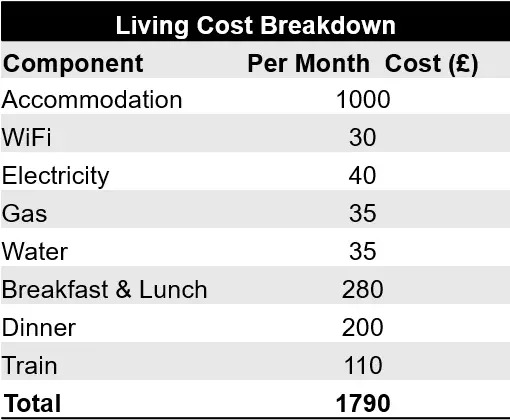

How much will you be able to save and spend? To answer these questions and boil the salary down to a more useful picture of what these earnings relate to, here is a simple breakdown of the living costs you might expect, living and working in Central London:

Explaining the assumptions:

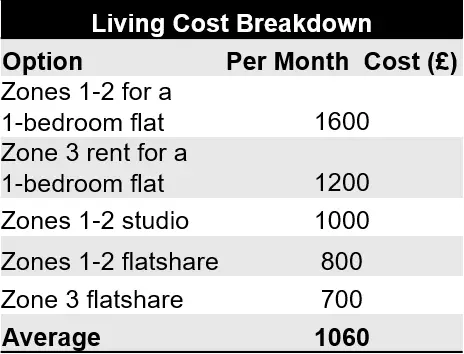

For accommodation, £1000 is a rounded down value from the mean of the various options available to someone looking for a place in central London according to this article. If you currently live beyond zone 3 or 4, renting a place more central is commonly seen as the most viable option. Personally, I commuted just under 1hr each way during my internship, but I know this would have been impossible as a full-time analyst, and that extra 30 minutes each way can massively contribute to the proportion of sleep you’re getting, especially when the waves of work increase in intensity.

WiFi, electricity, gas and water were also taken from the article linked above within the paragraph on accommodation.

Breakfast and lunch are calculated under the simple assumption that you might spend £10 a day on them combined, for 7 days a week (10*7*4=280). Most days, you can expect to be in the office when you’re eating dinner, and firms will usually pay for this. However, you might eat out once a week on average, and when including grocery shopping for weekend meals, I counted this as £50 a week (50*4=200).

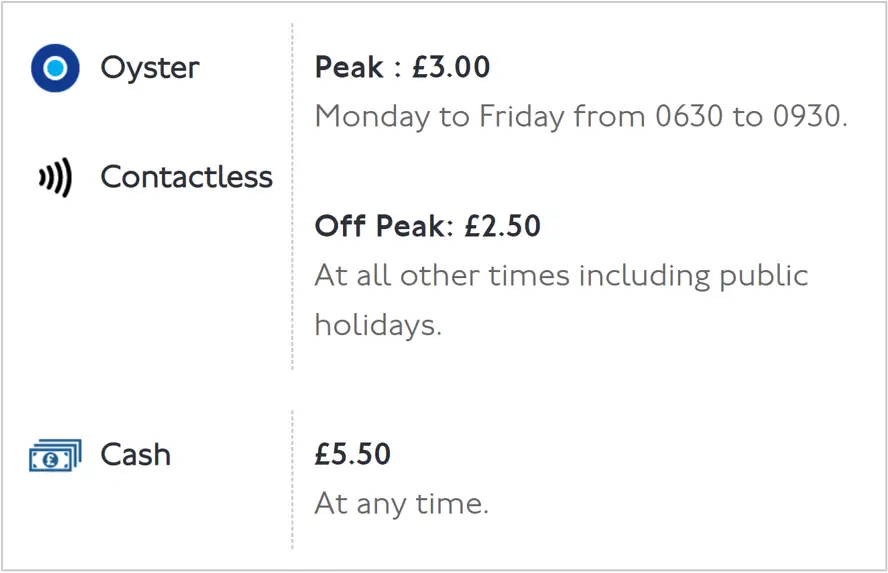

Finally, the following image, taken from the TFL rail website, shows how much it would cost during peak and off-peak times to travel from Stratford (zones 2/3) to Oxford Circus (zone 1).

I have assumed one journey during peak time in the morning and one journey off-peak since it is unlikely you’ll ever come home during ‘normal’ working hours ((3+2.5)*5*4). The extra £2.50 per day may be knocked off if you use an Uber that your company pays for when going home.

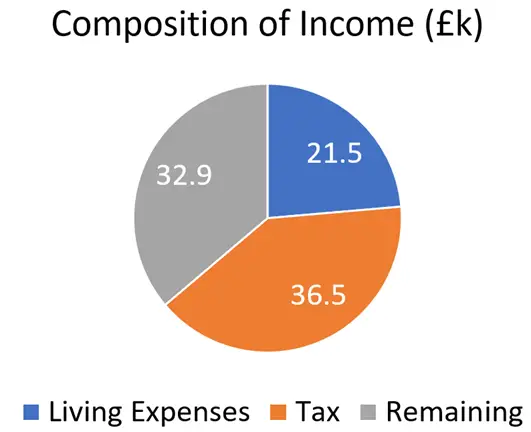

Taking into account these living costs per month, here is a breakdown of the total average salary:

‘Remaining’ income is what is left after taxes and estimated living expenses have been paid. In other words, you can do what you want with this remaining money, whether scaling up your life (not recommended) or investing for the future where you’ll have to report to your Chief Compliance Officer unless it’s an index fund or crypto since that’s still unregulated.

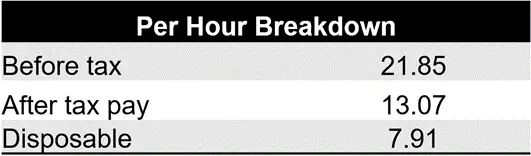

Per Day and Per Hour

The total breakdown is only useful in terms we can easily grasp, so here is a breakdown per day and per hour:

I have calculated these hourly figures assuming 16 hours per day, 5 days a week – some may dispute these figures for investment banking, but this is intended to be an average over a whole year.

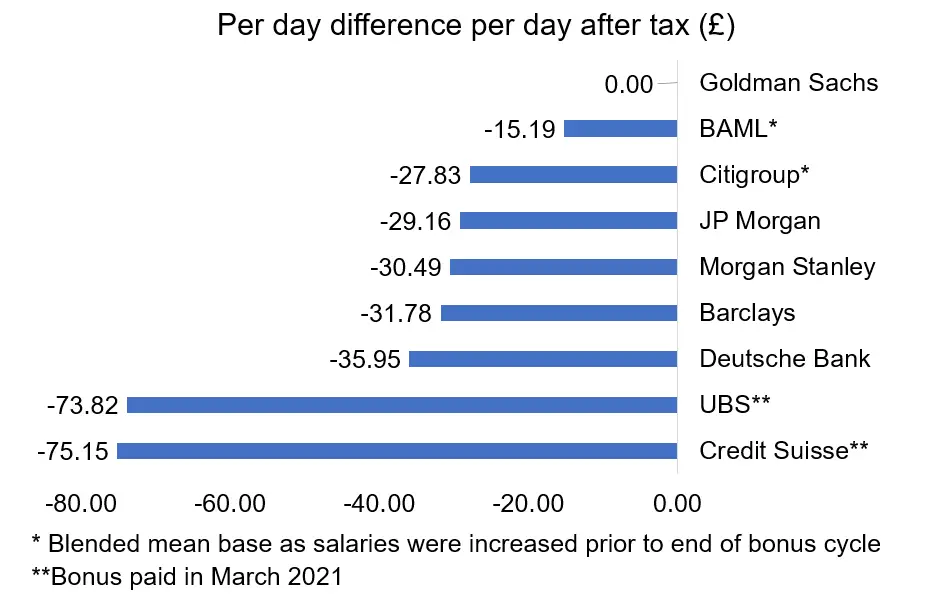

Not all Banks are Equal – Beyond the Salary

Firstly, I have illustrated the differences in pay between banks before making the more important point that there are many other qualitative factors that might make working at one bank much more desirable than another regardless of marginal pay differences.

The graph below depicts the after-tax difference between the highest paying bulge bracket and all the others according to the Dartmouth Partners report. Remember the important caveat that these figures may not be 100% accurate and are changing frequently. Also, remember that UBS and Credit Suisse data points were taken much earlier during March 2021.

Fine, we know that salaries clearly vary between banks and during the dislocation of increasing salaries, the variation between banks is going to increase as well. But what about beyond salaries? Lifestyle differences, level of toxicity and friendliness in the firm culture are very tangible factors that influence your satisfaction and quality of life on the job. I don’t want to talk badly about certain firms, since it is not my place to do so, but I strongly recommend networking with analysts and more senior people at the company to find out about such qualitative factors. Appreciating these qualitative factors is especially important if you feel disheartened that someone at another bank is supposedly getting a much ‘better deal’ than you.

Why London Firms Pay Less than US firms

When looking at the average investment banking salaries from sites like the Corporate Finance Institute (CFI), you may notice that US salaries are higher than London ones. CFI quote that a US-based analyst can expect to earn $125k-200k in total compensation, which translates to around £94k-150k as of December 2021. This compares to the £90k-122k quoted above from the Dartmouth Partners report for the majority of London investment banks.

Two reasons may have contributed to this discrepancy:

- Lifestyle differences. Holidays and free time, although still abnormal relative to most industries is comparatively better for UK-based investment bankers than for their counterparts in the US.

- Exchange rate fluctuations. The GBP has weakened against the USD over the last decade or so and when salaries at large banks were set in the past, they were based on a much stronger pound which may have contributed to the discrepancy.

Things to Bear in Mind when Considering Investment Banking

Caveat 1 – don’t just do investment banking for the money.

If you’re contemplating whether investment banking is the career you want to break into and salary is the number one factor driving you, I believe it’s worth first re-evaluating why that is the case, and realising there are probably ‘more efficient’ routes you should consider before investment banking.

Firstly, when confronting the notion that salary must be your top priority, I strongly recommend reading the part of the 4hr Work Week which talks about ‘definition’ where Tim Ferriss discusses the importance of finding out just how much we need to earn to become independent of our financial situation – it is probably lower than most of us think.

Secondly, on whether investment banking is for you if money is the main driving factor: It is true that a career in investment banking could lead you with several hundred thousand pounds stored up in investment or savings 4-5 years down the line. But unless you stay in the industry for well over a decade and reach to Managing Director level, where salaries are largely dependent on deals you lead for the firm, it is easy to overestimate how much you can make in the industry.

Thirdly, if you’re driven by the idea of financial independence, remember that a higher salary comes with a greater risk of wanting to scale up life expenses – this is very difficult to counteract and may lead to feeling more trapped than before starting full-time work. When someone is on a high salary and everyone around them is spending more on nicer accommodation, more expensive fashion, expensive restaurants, gadgets and the like, it is easy to see how a career that was supposed to bring more financial independence might create financial isolation.

Caveat 2 – don’t limit your options to Investment Banking.

If you’re mapping out the first part of your career and haven’t taken inventory of alternative routes, it might be worth checking out proprietary trading (trading in financial markets to make a profit using the firm’s assets), quant funds, corporate real estate, consulting, software engineering in a Big Tech company or a role in a booming Fintech firm. These alternative career paths overcome some of the downsides of IB while sharing some of the benefits – as a side note, the investment banking division does not offer the highest salary among these alternative options. On the other hand, you can never be certain about the future and perhaps the Big Tech scene will soon change or be broken up in an unrecognisable manner. Another career path you may consider is a more independent self-employment trajectory where you move into entrepreneurship and create alternative sources of income, although this is probably much easier said than done.

Caveat 3 – the industry comes with a lot of uncertainty.

Another caveat is that the industry comes with a lot of uncertainty. The recent increase in salaries is not a given in the industry and although tailwinds are supporting investment banking and M&A activity at the moment, this could easily pivot any time soon and as seen in previous episodes over the last couple of decades, investment banks are never the first to place the job security of its employees as a top priority.

Still interested in Investment Banking?

Taking into account those insights and caveats, if you’re still interested in pursuing a career in investment banking then be sure to check out the game plan summary for applying and landing a summer internship in the sector. This game plan is at the heart of this site and has one aim: to help you gain clarity on what can be such a challenging and competitive application process. The inspiration to make this game plan came when applying to internships myself and finding the power of clarity in reducing stress and making the process seem so much more possible – hopefully the divide and conquer strategy I follow in that game plan summary post will motivate you to keep pushing forward.

Happiness in Life – a final thought

As a final note, I found this TED Talk a fascinating, confronting perspective on whether investment banking is the right career. There are many benefits beyond the salary, such as a varied workflow, working with intelligent people, overcoming a steep learning curve that opens the door to many exit opportunities and helping clients at what is one of the most exciting parts of a business’s growth trajectory. However, like with everything in life, there are also downsides with the biggest perhaps being the lifestyle sacrifice. With lifestyle sacrifice comes relationship sacrifice which is where this TED Talk becomes more relevant.